Saving for Your Children’s Education – Investment Bonds

March 22, 2019

Australia has one of the highest levels of private school enrolment within the OECD countries¹. Our country also maintains one of the highest levels of private expenditure towards schools (i.e. contributions from households)². According to the Independent Schools Council of Australia, student enrolments in non-government schools are approximately 35% of the total school enrolments (but 41% in secondary school)³. The median fee of an Australian independent school is $5,100 per year⁴.

With housing affordability at a low and the high costs of education, some may be looking at commencing saving for educational purposes well in advance to give their child or grandchild a financial head start. One of the investment options for education savings is via an investment bond.

What is an investment bond?

An investment bond is a type of investment that is internally taxed at the company tax rate of 30%, rather than your own individual tax rate. With this type of investment, your money can be invested in a variety of investment options. You can access your money at any time and retain control over how your money is invested until it is transferred to your nominated beneficiary.

Investment Bonds may also provide estate planning benefits via nominating a beneficiary. This would mitigate the risk of the funds being distributed through the policy owner’s estate to other beneficiaries, against their wishes. You can nominate how it will be passed on to future beneficiaries without triggering a tax event. Also, if you were to die, all benefits are paid tax free to the recipients.

Investment Bonds can be structured to be creditor protected, so in the event of bankruptcy, you will have the funds from a bond to fall back on.

With Investment Bonds, there is no need to provide a TFN and no annual tax reporting is required unless a withdrawal is made within the first 10 years, making this a simple investment choice. After 10 years, your investment earnings won’t attract any personal tax, which is known as the 10-year rule. If a withdrawal is made within 10 years of the bond’s establishment, some or all the growth that has accumulated needs to be declared in the investor’s tax return. However, a tax offset will be available for the amount of tax that has already been paid.

Additional contributions can be made at any time into the bond. However, contributions can be no more than 125% of the value of the contributions made during the previous 12-month period. If the 125% rule is breached, the 10-year period during which withdrawals are taxable re-commences from the beginning of the year in which the breach occurs.

How can it help me save?

An investment bond could be a powerful savings tool, especially for those on higher marginal tax rates. If you are paying more than 30% tax per annum, then investing via an investment bond can be tax effective. Once you start to generate income over $37,000 p.a. you begin to pay 34.5% (including Medicare Levy) for every dollar earned, and this tax rate continues to increase up to 47% (including Medicare Levy) as your income grows.

A way to save on tax

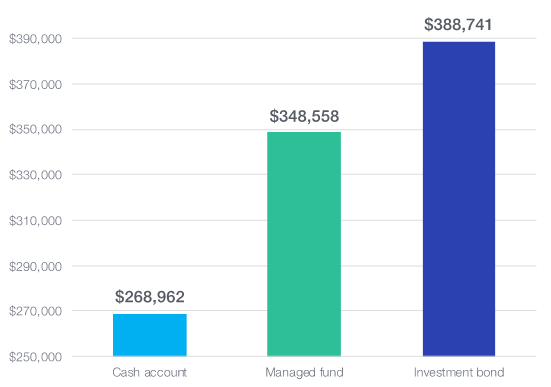

If your marginal tax rate is higher than 30%, an investment bond can allow your savings compound more tax effectively over time to give your child/grandchild a strong head start. This is demonstrated in the graph below.

Assumptions: $50,000 initial contribution; cash account investment pre-tax return of 3.2% p.a.; Managed funds and investment bond long term pre-tax return of 9.0% p.a. (5% income, 4% capital growth); Investment marginal tax rate of 47% (including Medicare Levy); $1,000 additional deposits per month; Investment held for 15 years.

Source: Generation Life

Is investment bond the right solution for me?

While an Investment Bond could be a tax-effective option for education savings, it may not be the best option for everyone. For someone on lower tax rates, a simple managed investment may be a more suitable option. Some may also benefit from the additional benefits that an Education Bond may offer. For grandparents, superannuation is another possible saving option.

There is no one-fit-all solution for education savings, and the best option depends on individual circumstances and needs. If you would like to discuss how you can save for your children’s/grandchildren’s education, please give us a call on 07 4638 2081 or drop us an e-mail on info@aspirefc.com.au.

- OECD (2011), “Private schools: Who Benefits?”, PISA in Focus, No. 7, OECD Publishing, Paris.

- OECD (2018), Education at a Glance 2018: OECD Indicators, OECD Publishing, Paris.

- ISCA (2018), Snapshot 2018, Independent Schools Council of Australia, Deakin.

- ISCA (2018), Independent Schools at a Glance 2018, Independent Schools Council of Australia, Deakin.